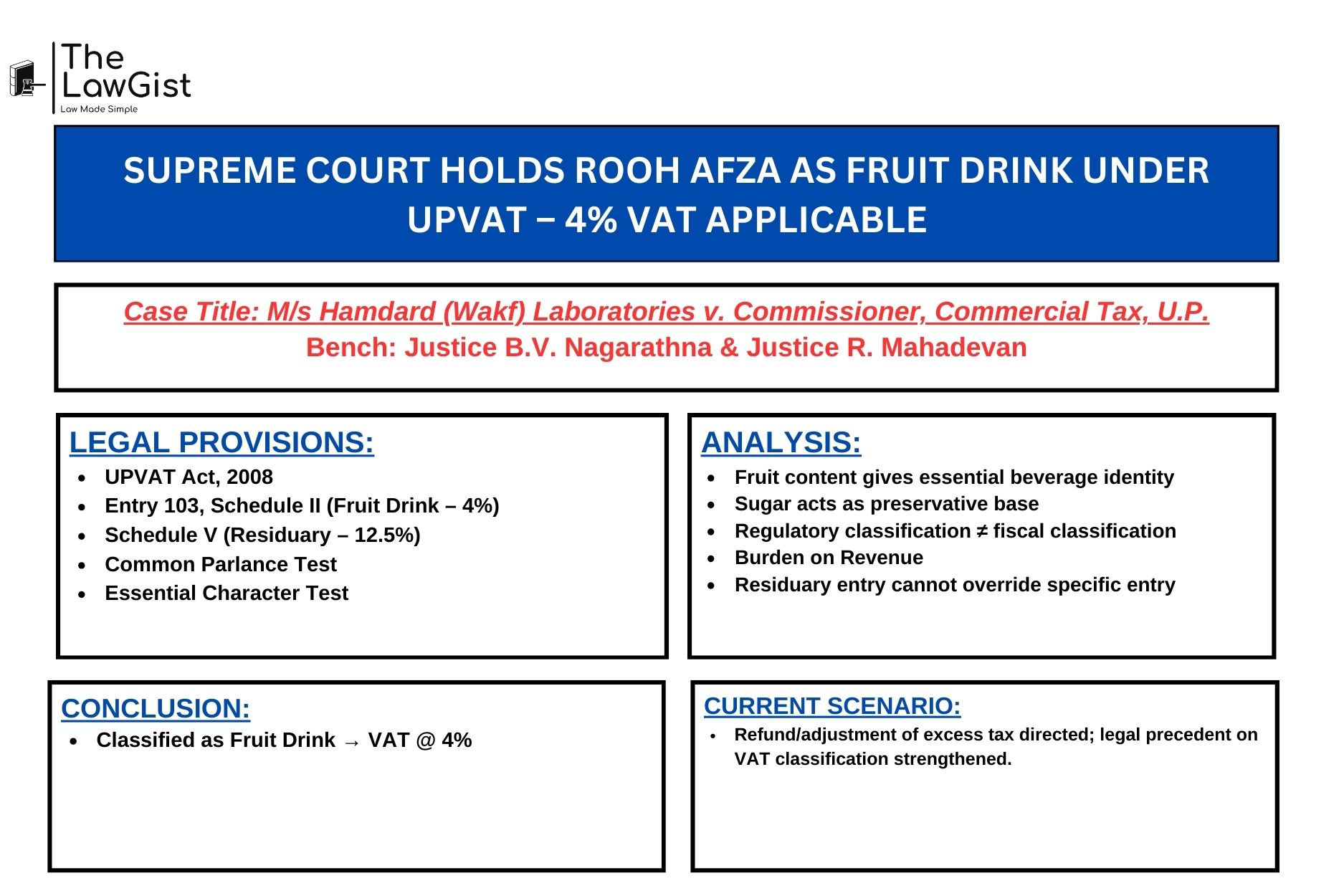

SUPREME COURT HOLDS ROOH AFZA AS FRUIT DRINK UNDER UPVAT – 4% VAT APPLICABLE

CASE SUMMARY – The Supreme Court in M/s Hamdard (Wakf) Laboratories vs. Commissioner, Commercial Tax, U.P. (2026) held that “Sharbat Rooh Afza” is classifiable as a “fruit drink” under Entry 103 of Schedule II of the UP VAT Act, taxable at 4%, and not under the residuary entry taxable at 12.5%. Applying the common parlance and essential character tests, the Court ruled that the product’s beverage identity derives from its fruit content despite high sugar composition. Regulatory food labeling norms cannot control fiscal interpretation. The Revenue failed to discharge its burden to justify classification under the residuary entry. The appeals were allowed with consequential refund relief.

| Particulars | Details |

| Case Title | M/s Hamdard (Wakf) Laboratories vs. Commissioner, Commercial Tax, U.P. |

| Introduction | The case concerns VAT classification of “Sharbat Rooh Afza” under the UPVAT Act, 2008 — whether taxable at 4% as “fruit drink” under Entry 103 Schedule II or 12.5% under the residuary entry Schedule V. |

| Factual Background | The appellant manufactured “Sharbat Rooh Afza” containing 10% fruit juice and paid VAT @4% treating it as “fruit drink.” The Department reclassified it as an unclassified item taxable @12.5%. The High Court upheld the Department’s view. |

| Legal Issues |

|

| Applicable Law |

|

| Analysis | The Court applied:

The product derived its essential character from fruit content and beverage identity, not sugar base. Regulatory labeling does not control fiscal classification. |

| Conclusion | “Sharbat Rooh Afza” is classifiable as “fruit drink” under Entry 103 Schedule II and taxable at 4%. High Court judgment set aside. |

| Current Scenario | Appeals allowed. Excess VAT paid @12.5% to be refunded/adjusted. The ruling clarifies classification principles for fruit-based beverage concentrates under VAT regime. |

“When a product reasonably fits within a specific entry, it cannot be relegated to the orphanage of the residuary clause.”

SOURCE – SUPREME COURT OF INDIA

Discover insighs on Latin Maxims and Legal Glossary and simplify complex legal terms in seconds.The LawGist ensures exam success with quality Blogs and Articles on — Top Legal Picks (TLP), Current Affairs, latest Supreme Court judgments as Courtroom Chronicles. Backed by trusted resources and videos, The LawGist is every Professionals and Aspirant’s first choice. Discover more at thelawgist.org