Legal steps to register and launch a business in India – from company structure to government compliance.

To start your own business in India is both thrilling and staggering. As passion and purpose are your driving forces, a solid legal checklist secures your startup business in India. Whether you’re launching a tech startup or a boutique café, navigating India’s legal landscape is important and there is a portal for starting a business under Startup India initiative by the government.

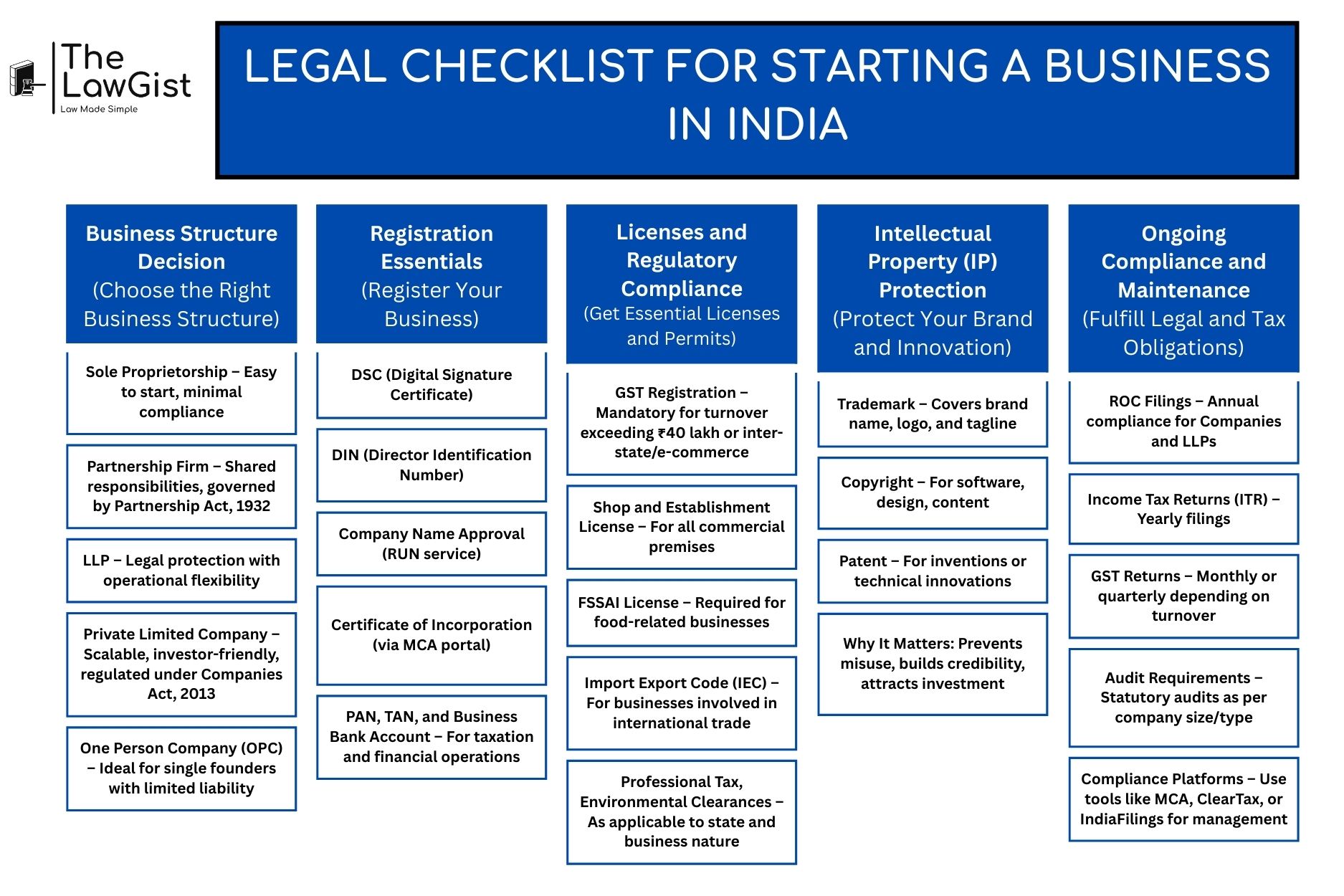

1. Choose the Right Business Structure

The first legal step you’ll make is analysing your business structure. Your choice will impact your taxes, liabilities, funding options, and even your exit strategy.

Common Structures in India:

- Sole Proprietorship: Simple and best for solo ventures. No separate legal entity.

- Partnership Firm: Shared ownership. Governed by the Indian Partnership Act, 1932.

- Limited Liability Partnership (LLP): Combines flexibility of a partnership with limited liability.

- Private Limited Company (Pvt Ltd): Preferred by startups for scalability, funding, and limited liability. Regulated by the Companies Act, 2013.

- One Person Company (OPC): Ideal for single founders wanting limited liability.

2. Register Your Business

Once your structure is finalized, get your business legally registered. Here’s what that typically includes:

- Digital Signature Certificate (DSC) – For filing forms electronically with the MCA.

- Director Identification Number (DIN) – Required for company directors.

- Company Name Approval – Done via the RUN (Reserve Unique Name) service on the MCA portal.

- Certificate of Incorporation – Issued after successful registration.

This process can take anywhere from 7 to 15 days, depending on how prepared you are with the documents.

3. PAN, TAN & Bank Account

Permanent Account Number (PAN) is mandatory for tax filings, and a Tax Deduction and Collection Account Number (TAN) is required if you’re deducting TDS.Once you have the PAN, you can open a current account in your business name.

4. Application for GST Registration

If your business turnover exceeds ₹40 lakh (₹20 lakh for NE and hill states), you need to register for GST (Goods & Services Tax). It’s also mandatory for e-commerce businesses or if you’re selling inter-state.

Even if not mandatory, GST registration can:

- Increase your credibility

- Allow input tax credit

5. Shops & Establishment License

Whether you’re opening a café or a co-working space, you need to register under your state’s Shops and Establishment Act. It governs working hours, holidays, wages, and safety.This license is generally obtained within 30 days of starting the business. Apply through the GST portal.

6. Necessary Licenses and Permits

Depending on the nature of your business, you may need sector-specific licenses. Here are some common ones:

| Type of License | Who Needs It | Where to Apply |

| Shop & Establishment License | All businesses with a physical office/shop | Local Municipal Corporation |

| FSSAI License | Food businesses | https://foscos.fssai.gov.in/ |

| Import Export Code (IEC) | Businesses importing/exporting goods | DGFT |

| Professional Tax | Required in some states | State tax department |

| Environmental Clearance | Industries affecting environment | State Pollution Control Board |

Each license may have a different validity period, so keep track of renewal dates.

7. Intellectual Property Protection

Got a catchy brand name, innovative software, or proprietary design? Protect your IP.

- Trademark: Protects brand name, logo, tagline

- Copyright: For creative works like software, content, and design

- Patent: For inventions or innovative processes (more complex and costly)

Registering your IP gives you legal recourse if someone tries to copy your work.

8. Maintain Compliance

In India businesses are required to file regular returns, maintain books of accounts, and conduct board meetings (for companies).

You may need:

- Annual ROC filings (for companies and LLPs)

- Income tax returns

- GST filings (monthly/quarterly)

- Audit reports

9. Annual Compliance

Compliance doesn’t stop after incorporation. Regular filings are crucial.

- Companies and LLPs must file annual returns with the MCA

- Income Tax Returns (ITR) must be filed yearly

- GST Returns (monthly or quarterly depending on turnover)

- Statutory audit (depending on company type and revenue)

Non-compliance can lead to heavy penalties and even business shutdown.

Conclusion -Your Legal Roadmap = Your Launchpad

Starting a business in India is like setting out on an epic journey. The process may be rough, but the right legal preparation gives you direction. The government is increasingly digitalizing and simplifying processes, but having a legal expert guide you—especially during setup—can save you headaches later.

Your dream deserves the right foundation. Start smart. Start legally.

SOURCES

ALSO READ- DIGITAL SIGNATURE VS PHYSICAL SIGNATURE: WHICH HOLDS MORE LEGAL WEIGHT?